Source image: Presentation B. Florian (9 juni 2023)

Scope of application & timing

"The reporting requirements will be phased in over time for different kinds of companies. The first companies will have to apply the standards in financial year 2024, for reports published in 2025. Listed SMEs are obliged to report as from 2026, with a further possibility of voluntary opt-out until 2028, and will be able to report according to separate, proportionate standards that EFRAG will develop next year." (source: efrag.org)

Educational videos on the first set of draft ESRS

EFRAG introduces the (first draft) ESRS in a series of educational videos: "This series of educational videos on the First set of draft ESRS provides interested stakeholders with an introduction to the draft standards. For each standard, our sustainability reporting experts offer you a choice of the glimpses, which will give you a brief overview, or the educational session for more technical details." (source: efrag.org). Here you can find the first educational video, the rest can be found on the EFRAG website:

Watch this video externally on:

YouTube

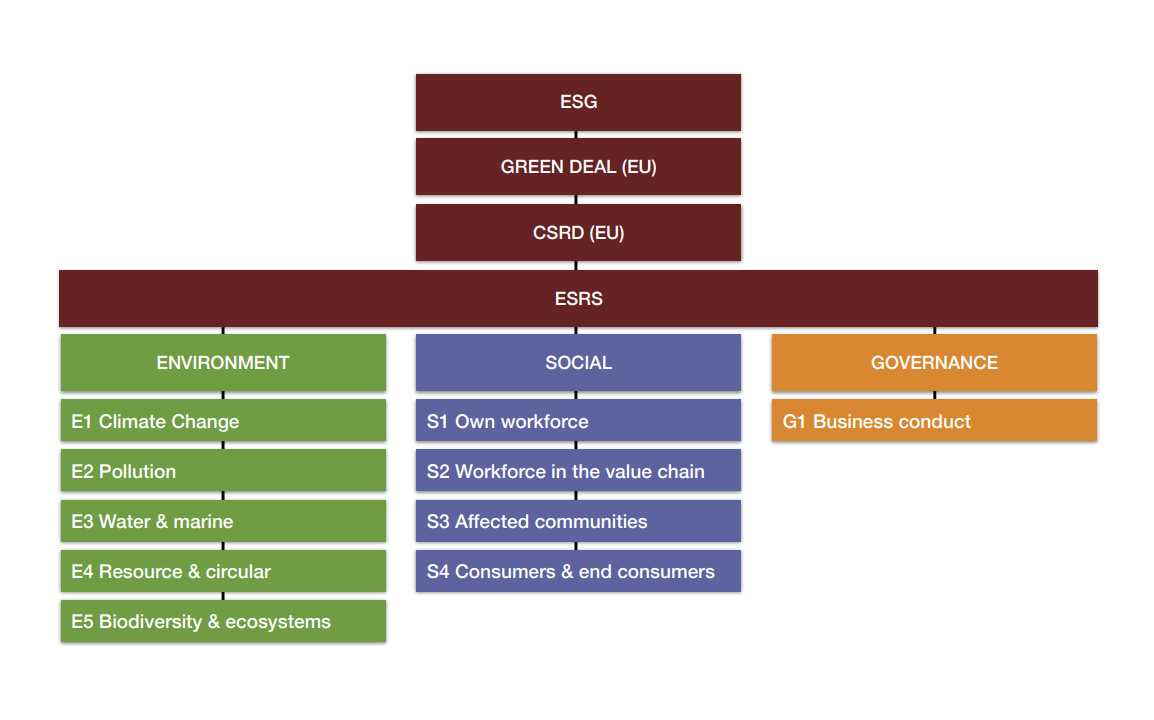

Legislative proposal for a Corporate Sustainability Reporting Directive (CSRD), adopted by the European Commission (source: eur-lex.europa.eu):

"EFRAG is a private association established in 2001 with the encouragement of the European Commission to serve the public interest. EFRAG extended its mission in 2022 following the new role assigned to EFRAG in the CSRD, providing Technical Advice to the European Commission in the form of fully prepared draft EU Sustainability Reporting Standards and/or draft amendments to these Standards. Its Member Organisations are European stakeholders and National Organisations and Civil Society Organisations. EFRAG’s activities are organised in two pillars: A Financial Reporting Pillar: influencing the development of IFRS Standards from a European perspective and how they contribute to the efficiency of capital markets and providing endorsement advice on (amendments to) IFRS Standards to the European Commission. Secondly, a Sustainability Reporting Pillar: developing draft EU Sustainability Reporting Standards, and related amendments for the European Commission." (source: efrag.org)